![]()

Introduction:

Directors and Officers insurance is also known as D&O Liability Insurance. This is coverage provided to directors, managers, etc. of a company that has a chance of being sued by a claimant. They also need protection from such liabilities which they face while serving as an officer or director of a business.

Such insurance covers legal fees, settlement, and costs that may occur as a result of the suit. D&O insurance is a reimbursement or indemnification made for losses or advancement of defense costs in the event an insured suffers such a loss as a result of a legal action brought for alleged wrongful acts in their capacity as directors and officers.

These covers are taken by companies because managers and directors are human too, they can also make mistakes. Such coverages do not include fraudulent, criminal, or intentional non-compliant acts or cases where directors obtained illegal remuneration or acted for personal profit.

Who are Officers and Directors?

- An individual who has been recorded as a director in the public outline given by the Company.

- The representative of the organization, who had in the past been or in the present is an individual from the corporate general advice of the policyholder.

- An individual who, in the past has been or in the present is a shadow chief or true overseer of the organization.

- Any individual, who has been previously, or in the present is or will be later on the chief, administrative board part, the executives’ council part, official, the executives board part or Governor of the organization who has been properly chosen by law.

Need for Insurance

- In case of accounting irregularities

- To regulate investigation

- To comply with legal necessities

- In case of breach of obligation leading to bankruptcy or loss

- Misuse of assets of the company

Features of D&O Insurance

- It shields the organization or association from any kind of lawful liabilities that may emerge if a chief or official blunders any obligation prompting a huge misfortune for the organization.

- In such a manner, it ought to be referenced that this sort of protection strategy avoids harm of property and real injury, separation and untruthfulness by the safeguarded, criticism of character, and infringement of the laws as set somewhere near Liability Insurance India.

- The cases of risk must be covered in case they are made within the time span of the arrangement. There is a specified period for every approach, which can be stretched out as long as 72 months.

- Normally, these don’t contain any express obligation to shield the people who have been protected.

- Any kind of property harm is likewise excluded from the protection strategy.

Types

- SIDE A: this protects the assets of individual directors and officers for claims where the company is not legally or financially able to fund indemnification.

- SIDE B: This reimburses public or private companies to the extent that it grants indemnification and advances legal fees on behalf of directors/officers.

- SIDE C: It extends cover for a public company (the entity, not individuals) for security claims only.

Chiefs and officials are stood up to with an expanding hazard that their organization will most likely be unable to repay them for misfortune. An additional layer of the guard to individual assets can be gotten by buying Side A cover, which guarantees chiefs and officials just (not the organization) when repayment is inaccessible.

Frequently insufficient inclusion is purchased for the danger, so a significant pattern is for more Side A cover to be bought all together for a singular official to secure individual resources. D&O cover has turned into an ordinary cover for huge worldwide organizations, yet all sizes of associations – public, private, or non-benefit – have likely openings.

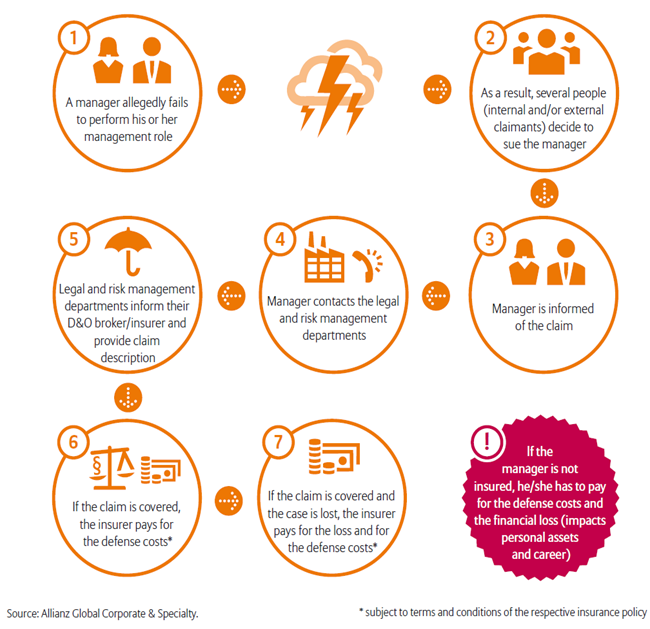

How does D&O Insurance Work?

Everything begins when a manager or director supposedly neglects to play out their job. Some normally dangerous situations incorporate work negligence, revealing blunders, mistaken exposures, bankruptcies, and guideline infringement. Thus, a few claimants choose to sue the administrator.

When the administrator and the legal risk executives, divisions are educated regarding the case, they then, at that point, give a depiction of the case to their insurer. If the case is covered, the insurer takes care of the safeguard costs. If the claim is covered and the case is lost, the guarantor pays for the safeguard costs and the monetary misfortunes.

Advantages of D&O Insurance

- In the event that an association faces misfortunes because of an incorrect choice or activity taken by the administrative board as well as the chiefs and officials, according to the articles and updates of the affiliation.

- With the assistance of this protection plan, repayment can be given to the lawful beneficiary or lawful agents of the official or chief, in the event that he is delivered indebted and bankrupt.

- Every one of the lawful costs that will result from the arraignment of the chief and official will be completed with the composed assent of the protection supplier.

- Reasonable goals to the cases are given by the protection which infers that there is a shot at getting full inclusion in specific cases.

- Protection costs are additionally remembered for the arrangements and this cover doesn’t lessen the general furthest reaches of the obligation as determined in the approach.

- Every one of the guaranteed people under this strategy is qualified to cover against instances of lewd behavior, illegitimate end, oppressive demonstrations, and different demonstrations that may bring about misfortune to the association.

- Other than securing the officials and chiefs, it gives a cover to the actual organization.

- You will have the option to cover a wide assortment of cases by contributing a generally low measure of cash.

Conclusion

D&O has since a long time ago become a standard item for huge partnerships. The cover is important to empower troughs to convey choices without the intimidation of individual risk continually looming over them. Rather than being compelled to secure their vocation by battling each and every case through the courts, this sort of cover empowers supervisors to settle these cases rapidly and generally watchfully. However, regardless of whether a backup plan at last probably won’t cover a misfortune, D&O protection will be helpful in light of the fact that the safeguard costs for the case can likewise be covered.

In the present progressively globalized markets, it is turning out to be increasingly more significant for the safety net provider to likewise be all around the world organized. The safety net provider needs to see each legitimate climate in which the customer is dynamic, and the nearby approaches need to reflect the neighborhood conditions. Above all, the guarantor should have the option to oversee claims worldwide and set up a worldwide program that gives facilitated worldwide inclusion. D&O will unquestionably stay a subject of public conversation throughout the planet. It is in the interests of the protection business, business customers, and specialists just as controllers and the press to proceed with this conversation and further foster this basic space of corporate danger cover.

D&O insurance is a great financial tool for reducing risk and giving your directors and officers the peace of mind to confidently make the needed, sometimes difficult decisions necessary to spark growth. It can also strengthen your financial planning by eliminating the fear that you’ll need a stockpile of funds to combat potential litigation.

{kind=link}

0 Comments